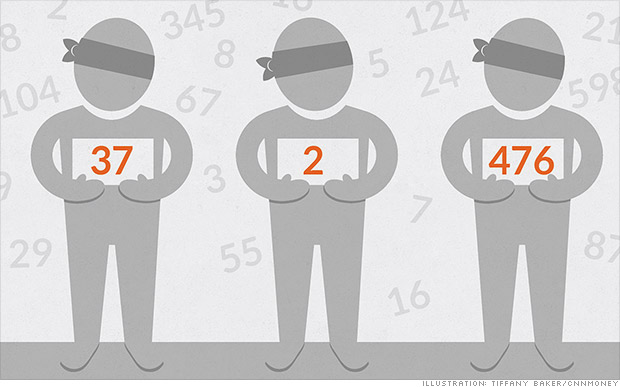

Justin Sullivan/Getty Images NEW YORK and DETROIT -- U.S. banks looking to get in on a booming market for financing new-car sales have run into a formidable competitor: the auto manufacturers themselves. Financing arms of car companies, including Toyota Motor (TM), Honda Motor (HMC) and Ford Motor (F), made half of all new U.S. car loans in the first quarter, up from 37 percent a year earlier and the largest percentage of the market in four years, according to credit data firm Experian (EXPR). These companies also write the vast majority of leases, which contributed a record 26 percent of new car sales in the quarter, up from 23 percent last year and 20 percent in 2012. The financing arms are providing subsidies from the manufacturers, lowering monthly payments and extending loan terms to make it easier for buyers to drive away in a shiny, new vehicle. As a result, major banks are increasingly moving into riskier parts of the market to make loans. U.S. Bancorp (USB), for example, for the first time ever decided to start financing used cars, an area of the market that the automakers' finance companies have little interest in. It also started offering loans to less creditworthy borrowers. And Wells Fargo (WFC) has been leveraging off a nationwide deal with General Motors (GM) to provide loans subsidized by the No. 1 U.S. automaker. Wells sees this as a way to gain more of the used car loan business at GM dealerships. The aggressive push by car companies is beginning to raise questions among industry analysts and consultants about whether it is sustainable. If interest rates rise, the automakers could find the incentives too costly unless they are prepared to take a hit to profits -- with any pullback in the deals being offered customers running the risk of hurting demand. And, if used car prices weaken, the financing units could be hit with losses on vehicles coming back from leases and repossessions. The automakers' financing companies are doing substantially more than they were just a year or two ago, said April Ancira, vice president in the San Antonio office of Ancira Motor, a Texas-based group with 11 dealerships selling GM, Nissan, Fiat, Chrysler, VW and Ford cars. "They're being very aggressive with incentives," Ancira said. Pete Carey, vice president for sales at Toyota Financial Services, said incentives are playing a bigger role as automakers look to stand out in a crowded market where the basic quality of cars is uniformly good. "We're at a point in the industry that we're spending as much as we've ever spent," Carey said. The strategy is currently paying off in spades for automakers. All the major automakers posted healthy profits in the first quarter. U.S. car sales rebounded in May to an annualized rate of 16.8 million vehicles, against 15.6 million for all of last year. Sales were only 10.4 million in 2009 as the recession crushed demand. Outstanding U.S. loans on new cars totaled $811 billion at the end of March, up 11.6 percent from a year earlier, according to Experian. Fears of Used-Car Glut The automakers are in a position to offer the deals because their cost of borrowing has gone down as their balance sheets have improved and as bond investors have lined up to buy securities backed by loans and leases. But they risk sweetening the deals so much that it starts to cut into their profit margins. In a few years time, as the leased vehicles are returned, the strategy could lead to a glut in the used-car market. If a car turns out to be worth less at the end of a lease than projected, the finance company will take a loss on the lease, said Jim Ziegler, a consultant to car dealers. "It appears as a profit until they get the car back," Ziegler said. Analysts at Moody's Investors Service said car resale values at the end of leases have so far tended to be higher than assumed, resulting in double-digit gains for finance companies and lease investors. But the gains have started to decelerate to single-digits now and they expect to see that downward pressure continue this year. "There is still room for used car prices to decline before we see any losses," said Aron Bergman, of Moody's. But, he added, "the gains are going down." Sweet Subsidies The average monthly lease payment for the most-leased car in America, the Honda Civic, was $251 in the first quarter, according to Experian. But when Jonathan Stierwald, a Minnesota resident, wanted to lease a car for his nephew, he found Mike Piazza Honda in Pennsylvania willing to lease him the car for three years for just $80 a month. He flew there to get the deal. The lease was financed by Honda's finance arm. The details of the deal could not be determined. A salesman at the Langhorne, Pennsylvania dealership, which is owned by Piazza, the former All-Star baseball catcher, said factors such as a high credit score and higher down-payment may have helped. Honda representative Steve Kinkade said the dealership could have added its own incentives on top of the company's promotions. Honda, which was fifth in U.S. auto sales in the first five months of the year, increased its average subsidy per leased car by 26 percent to $1,476 in that period from a year earlier, according to Edmunds.com. Kinkade said the company is pleased with how its finance unit has paced its leasing to drive sales without too many of the cars later coming onto the used car market and depressing prices. Others are liberally using subsidies, too. Toyota subsidized 92 percent of its U.S. leases in its fiscal year ending in March, up from 82 percent the year before. "We can get fairly aggressive with pricing or payments, depending on what we anticipate the used market to look like," Toyota's Carey said. Auto industry analysts and consultants said they did not think the situation was getting out of hand just yet. The average incentive per car sold so far this year was $2,918, up slightly from $2,825 a year earlier and just under 10 percent of the average transaction price, according to J.D. Power & Associates data. Banks In Used-Car Lots Automaker finance arms are also offering loans at interest rates as low as zero percent. And, they are taking on more loans to borrowers with subprime credit ratings, according to data from Experian. The length of loans is also increasing. Lenders granted one-in-four new car buyers more than six years to repay in the first quarter, up from one-in-five a year earlier, the figures show. The average monthly payment on new car loans was $474 in the first quarter, only $15 more than a year earlier, even as the average amount financed rose by $964 to a record $27,612. Unable to compete, some banks are in retreat. Ally Financial (ALLY), which was once GM's financing arm but is now on its own, increased its financing of used car purchases by 14 percent in the first quarter from a year earlier, but its new car lending declined so much that it made 6 percent fewer auto loans in total. U.S. Bancorp estimated that used cars will eventually make up 40 percent of its auto loans after doing none in the past. Consumers with "nonprime" credit scores, defined as below 675, will account for 15 percent of U.S. Bancorp's portfolio, compared with none previously. Not that the opportunity in the used car market isn't also large -- in terms of numbers of vehicles sold the used car market is more than twice the size of the new-car market. Tom Wolfe, executive vice president of consumer credit solutions at Wells Fargo, said its partnership with GM improves its ties with dealers and that for every subsidized new car loan it makes for GM at a dealer it will pick up three used-car loans. Wells Fargo is the largest U.S. used-car lender with a 7.1 percent market share, according to Experian. Wolfe said customers who borrow to buy a used car so that they can get to and from work are good credit risks. -.

Justin Sullivan/Getty Images NEW YORK and DETROIT -- U.S. banks looking to get in on a booming market for financing new-car sales have run into a formidable competitor: the auto manufacturers themselves. Financing arms of car companies, including Toyota Motor (TM), Honda Motor (HMC) and Ford Motor (F), made half of all new U.S. car loans in the first quarter, up from 37 percent a year earlier and the largest percentage of the market in four years, according to credit data firm Experian (EXPR). These companies also write the vast majority of leases, which contributed a record 26 percent of new car sales in the quarter, up from 23 percent last year and 20 percent in 2012. The financing arms are providing subsidies from the manufacturers, lowering monthly payments and extending loan terms to make it easier for buyers to drive away in a shiny, new vehicle. As a result, major banks are increasingly moving into riskier parts of the market to make loans. U.S. Bancorp (USB), for example, for the first time ever decided to start financing used cars, an area of the market that the automakers' finance companies have little interest in. It also started offering loans to less creditworthy borrowers. And Wells Fargo (WFC) has been leveraging off a nationwide deal with General Motors (GM) to provide loans subsidized by the No. 1 U.S. automaker. Wells sees this as a way to gain more of the used car loan business at GM dealerships. The aggressive push by car companies is beginning to raise questions among industry analysts and consultants about whether it is sustainable. If interest rates rise, the automakers could find the incentives too costly unless they are prepared to take a hit to profits -- with any pullback in the deals being offered customers running the risk of hurting demand. And, if used car prices weaken, the financing units could be hit with losses on vehicles coming back from leases and repossessions. The automakers' financing companies are doing substantially more than they were just a year or two ago, said April Ancira, vice president in the San Antonio office of Ancira Motor, a Texas-based group with 11 dealerships selling GM, Nissan, Fiat, Chrysler, VW and Ford cars. "They're being very aggressive with incentives," Ancira said. Pete Carey, vice president for sales at Toyota Financial Services, said incentives are playing a bigger role as automakers look to stand out in a crowded market where the basic quality of cars is uniformly good. "We're at a point in the industry that we're spending as much as we've ever spent," Carey said. The strategy is currently paying off in spades for automakers. All the major automakers posted healthy profits in the first quarter. U.S. car sales rebounded in May to an annualized rate of 16.8 million vehicles, against 15.6 million for all of last year. Sales were only 10.4 million in 2009 as the recession crushed demand. Outstanding U.S. loans on new cars totaled $811 billion at the end of March, up 11.6 percent from a year earlier, according to Experian. Fears of Used-Car Glut The automakers are in a position to offer the deals because their cost of borrowing has gone down as their balance sheets have improved and as bond investors have lined up to buy securities backed by loans and leases. But they risk sweetening the deals so much that it starts to cut into their profit margins. In a few years time, as the leased vehicles are returned, the strategy could lead to a glut in the used-car market. If a car turns out to be worth less at the end of a lease than projected, the finance company will take a loss on the lease, said Jim Ziegler, a consultant to car dealers. "It appears as a profit until they get the car back," Ziegler said. Analysts at Moody's Investors Service said car resale values at the end of leases have so far tended to be higher than assumed, resulting in double-digit gains for finance companies and lease investors. But the gains have started to decelerate to single-digits now and they expect to see that downward pressure continue this year. "There is still room for used car prices to decline before we see any losses," said Aron Bergman, of Moody's. But, he added, "the gains are going down." Sweet Subsidies The average monthly lease payment for the most-leased car in America, the Honda Civic, was $251 in the first quarter, according to Experian. But when Jonathan Stierwald, a Minnesota resident, wanted to lease a car for his nephew, he found Mike Piazza Honda in Pennsylvania willing to lease him the car for three years for just $80 a month. He flew there to get the deal. The lease was financed by Honda's finance arm. The details of the deal could not be determined. A salesman at the Langhorne, Pennsylvania dealership, which is owned by Piazza, the former All-Star baseball catcher, said factors such as a high credit score and higher down-payment may have helped. Honda representative Steve Kinkade said the dealership could have added its own incentives on top of the company's promotions. Honda, which was fifth in U.S. auto sales in the first five months of the year, increased its average subsidy per leased car by 26 percent to $1,476 in that period from a year earlier, according to Edmunds.com. Kinkade said the company is pleased with how its finance unit has paced its leasing to drive sales without too many of the cars later coming onto the used car market and depressing prices. Others are liberally using subsidies, too. Toyota subsidized 92 percent of its U.S. leases in its fiscal year ending in March, up from 82 percent the year before. "We can get fairly aggressive with pricing or payments, depending on what we anticipate the used market to look like," Toyota's Carey said. Auto industry analysts and consultants said they did not think the situation was getting out of hand just yet. The average incentive per car sold so far this year was $2,918, up slightly from $2,825 a year earlier and just under 10 percent of the average transaction price, according to J.D. Power & Associates data. Banks In Used-Car Lots Automaker finance arms are also offering loans at interest rates as low as zero percent. And, they are taking on more loans to borrowers with subprime credit ratings, according to data from Experian. The length of loans is also increasing. Lenders granted one-in-four new car buyers more than six years to repay in the first quarter, up from one-in-five a year earlier, the figures show. The average monthly payment on new car loans was $474 in the first quarter, only $15 more than a year earlier, even as the average amount financed rose by $964 to a record $27,612. Unable to compete, some banks are in retreat. Ally Financial (ALLY), which was once GM's financing arm but is now on its own, increased its financing of used car purchases by 14 percent in the first quarter from a year earlier, but its new car lending declined so much that it made 6 percent fewer auto loans in total. U.S. Bancorp estimated that used cars will eventually make up 40 percent of its auto loans after doing none in the past. Consumers with "nonprime" credit scores, defined as below 675, will account for 15 percent of U.S. Bancorp's portfolio, compared with none previously. Not that the opportunity in the used car market isn't also large -- in terms of numbers of vehicles sold the used car market is more than twice the size of the new-car market. Tom Wolfe, executive vice president of consumer credit solutions at Wells Fargo, said its partnership with GM improves its ties with dealers and that for every subsidized new car loan it makes for GM at a dealer it will pick up three used-car loans. Wells Fargo is the largest U.S. used-car lender with a 7.1 percent market share, according to Experian. Wolfe said customers who borrow to buy a used car so that they can get to and from work are good credit risks. -.

Wednesday, December 31, 2014

Automakers Driving Banks from Buoyant New Car Market

Tuesday, December 30, 2014

Euro drops; Draghi is ‘comfortable’ easing in June

NEW YORK (MarketWatch) — The euro dropped against the U.S. dollar Thursday after European Central Bank President Mario Draghi said he would be "comfortable" easing monetary policy further in June, if needed.

/quotes/zigman/4867933/realtime/sampled EURUSD 1.3839, -0.0072, -0.5182%

The euro (EURUSD) fell to $1.3851 from $1.3910 late Wednesday, giving up earlier gains. The euro had risen as high as $1.3995 after the European Central Bank held its interest rates steady , as expected.

During the subsequent press conference, Draghi said he would like to see the updated ECB staff projections in June before any decision to ease is made. He said the strengthening of the exchange rate is cause for "serious concern" in the context of low inflation, adding that the interest rate is not a policy target for the central bank. Read live blog recap: Draghi says 'comfortable with acting' in June if needed

Draghi's comments were more "aggressively dovish" than the market had expected, said George Dowd, head of Chicago foreign exchange for Newedge. While the market is likely to price in further easing next month, the type of easing remains uncertain. ECB officials have said they stand ready to pursue unconventional measures, such as quantitative easing or a negative deposit rate, in order to fight low inflation.

The ECB currently aims for inflation of just under 2% in the medium term as it sets monetary policy. "The targeting of negative interest rates is really a targeting of the exchange rates," said Sebastien Galy, senior foreign-exchange strategist at Societe Generale. "In a sense, if it goes for negative interest rates, it's almost as if the ECB implicitly adopts a dual mandate," he added.

AFP/Getty Images

AFP/Getty Images  Enlarge Image ECB President Mario Draghi's comments pushed the euro lower.

Enlarge Image ECB President Mario Draghi's comments pushed the euro lower. The euro on Thursday was at its lowest level against the dollar since April 29, according to FactSet.

The increased likelihood of further easing from the ECB next month comes as the Federal Reserve continues to reduce its stimulative bond purchases, which are on track to draw to a close by year end. Fed Chairwoman Janet Yellen on Thursday finished her two-day testimony to Congress about the economic outlook, in which she refused to give a timeline for when the Fed could begin to hike rates. Higher rates should make U.S. assets more attractive. Read: 3 of the most important things Yellen said Thursday

The ICE dollar index (DXY) , which measures the dollar's strength against six other currencies, rose to 79.433 from 79.238 late Wednesday. The WSJ Dollar Index (XX:BUXX) , an alternate gauge of dollar strength, was at 72.56 versus 72.54.

In the U.S., weekly jobless claims posted a bigger-than-expected drop to a seasonally adjusted 319,000.

Elsewhere in the market, the British pound (GBPUSD) fell to $1.6932 from $1.6955 late Wednesday. The Bank of England left rates on hold and made no change to the size of its bond-buying program, meeting expectations.

The dollar (USDJPY) fell to 101.57 Japanese yen from ¥101.90 late Wednesday. The Australian dollar (AUDUSD) rose to 93.73 U.S. cents from 93.28 U.S. cents.

More must-reads from MarketWatch:The next banking crisis is already in the making

'Comfortable' Mario Draghi just put ECB in corner

FXCM profit down 70% as trading revenue falls

Monday, December 29, 2014

Big Data is secretly scoring you

Marketers, banks and others could be using secret consumer scores to rank you.

NEW YORK (CNNMoney) You likely know about your credit score -- that key measure that influences everything from your monthly car payment to your ability to buy a home. But there are dozens of other consumer scores that are impacting your daily life that you have no idea about.Data brokers, analytics firms and retailers are creating hundreds of "secret" consumer scores that rank you on everything from the likelihood you will keep your job to how likely you are to commit fraud, according to a report released Wednesday by nonprofit World Privacy Forum.

Marketers, financial institutions, wireless phone service providers, law enforcement agencies and others use these scores to do everything from promoting new products to investigating crimes.

Yet, while these consumer scores are pervasive, most consumers don't know they exist. Rarely are they able to view their scores, find out how they are compiled or used or correct inaccuracies like they can on a credit report, the World Privacy Forum found.

"Consumers have little to no ability to learn when their lives are affected in a major or minor way by a consumer score that they never heard about," the report's authors Pam Dixon and Bob Gellman wrote. The two are calling for more transparency and government scrutiny of consumer scores.

Dixon and Gellman acknowledge that some scores could be used to help consumers, by providing them with targeted deals and discounts, for example. But they say some scores infringe on a consumer's privacy and can affect their eligibility for everything from a new job to affordable insurance. Inaccuracies could also cause a consumer to be mislabeled as a fraudster and shut out of important lines of credit.

"Whether a consumer receives a coupon for a free soda is not a big deal," they wrote. "Whether a consumer can complete a transaction is of significant consequence."

Here are just a few of the hundreds of scores that the World Privacy Forum uncovered:

Consumer profitability score: Using factors like your income, one company sells a score which predicts how likely you will be to pay your debts. The higher your score, the more likely you are to be a "profitable" customer (and a target of marketers).

Churn score: Many companies, such as wireless carriers and cable companies, create scores that predict how likely you are to take your business to a competitor. Get deemed a flight risk, and you may be offered a better deal. On the flip side, get labeled a stable customer and you may end up paying higher rates! .

Job security score: One company sells a score that uses employment and unemployment data, economic trends and forecasts to predict the probability that you will lose your job, and as a result not be able to pay your bills.

Banks sometimes use these lists in order to limit their losses, according to the report.

Medication adherence score: Do you always follow your doctor's orders? Or do you skip a pill here and there? One firm sells a score that predicts the likelihood you will follow a prescription plan, based on factors ranging from age to home ownership, that is designed to let pharmacies and insurers know when a patient is at risk and needs a medication reminder.

This data company knows all about you

This data company knows all about you As long as the score does not use your own protected health information, it would not be protected by privacy laws.

Fraud scores: Widely used by retailers, credit card issuers and other companies, fraud scores indicate whether a consumer may be posing as someone else or attempting to perpetuate a fraud of some sort.

While the scores are an important fraud and loss prevention tool, they can also create major headaches for any consumer who gets incorrectly labeled or is a victim of identity theft.

Get branded as a high risk and you could be declined on credit card purchases or rejected on loan applications, among other things. And unlike a credit score, you typically have few rights to access or contest a fraud score.

Custom scores: Some retailers create their own custom scores using sophisticated analysis of their massive databases of customer purchases and demographic information. The most famous example: Target's pregnancy predictor score, which used a consumer's shopping history to predict that she was pr! egnant ev! en before she had told family members.

Law enforcement scores: A variety of government scores are used for safety, anti-terrorism and other law enforcement purposes, but very little is known about how this information is used, the report stated. ![]()

Sunday, December 28, 2014

Most Generous 401(k) Plans in America

By Hal M. Bundrick

NEW YORK (MainStreet) Thank your employer for offering a 401(k) retirement plan. It's a big deal. And if you work for one of the companies listed below, you're receiving the most generous benefits available in the U.S. BrightScope, the financial benefits research firm, says these companies "value setting their employees up for a strong financial future."

The research firm examined plan vesting schedules, eligibility periods and all contributions to the plan made by the company for the sole benefit of the plan's participants. Companies in professional services, science and technical fields dominated, representing half of all the plans listed.

Six of the top 10 plans allow immediate vesting: workers are fully vested from the first day of employment. The average account balance for plans on the "most generous companies" list is $470,014 much higher than the average balance of all plans within the BrightScope system ($99,061). The average amount a company contributes to each plan on the list is $31,181, compared to the plan average of $4,184. And the average participation rate is 96.49% -- compared to an average of 85.03%. "Generosity is an important means for companies to recruit and retain top employees," says Brooks Herman, head of data and research at BrightScope. "Its importance is exemplified by the fact that half of the companies on this list have been on one or more other BrightScope rankings this year, and several more have been featured in years past." The 30 Most Generous Companies are: 1. Sullivan & Cromwell LLP - Retirement Plan of Sullivan & Cromwell LLP 2. North American Partners in Anesthesia, LLP - North American Partners in Anesthesia, LLP Profit Sharing Plan 3. Oregon Anesthesiology Group, P.C. - Oregon Anesthesiology Group, P.C. 401(k) Profit Sharing Plan 4. Frontier Refining & Marketing Inc. - Frontier Retirement Savings Plan 5. O'Melveny & Myers LLP - O'Melveny & Myers LLP Keogh Plan 6. Zeta Associates - Zeta Associates Incorporated Savings Plan 7. Shearman & Sterling LLP - Shearman & Sterling LLP Partners Retirement Plan 8. Anesthesia Service Medical Group, Inc. - Anesthesia Service Medical Group, Inc. 401(k) Profit Sharing Plan Trust 9. Cravath, Swaine & Moore LLP - Retirement Plan of Cravath, Swaine & Moore LLP 10. Bryan Cave LLP - Bryan Cave LLP Retirement Plan for Partners 11. Debevoise & Plimpton LLP- Retirement Plan for Lawyers of Debevoise & Plimpton LLP 12. Kay Scholer LLP - Kaye Scholer LLP Retirement Plan 13. Skadden, Arps, Slate, Meagher & Flom, LLP - Skadden, Arps, Slate, Meagher & Flom Retirement Plan 14. Deloitte LLP - Deloitte Profit Sharing Plan 15. United States Member Clubs of the National Hockey League - National Hockey League Pension Plan for Players of United States Member Clubs 16. Ernst & Young U.S. LLP - Ernst & Young Partnership Retirement Plan 17. Weil, Gotshal & Manges, LLP - Weil, Gotshal & Manges Partners' Target Pension Plan 18. Simpson Thacher & Bartlett LLP - Simpson Thacher & Bartlett LLP Supplemental Profit Sharing Plan for Partners 19. Jones Day - Jones Day Retirement Plan 20. Jennison Associates LLC - Jennison Associates Savings Plan 21. Duane Morris LLP - Duane Morris Retirement Plan 22. Dodge & Cox - Dodge & Cox Profit Sharing Plan & Trust 23. Sutter Medical Group, Inc. - Sutter Medical Group 401(k) Profit Sharing Plan 24. United Parcel Service Company - UPS/IPA Defined Contribution Money Purchase Pension Plan 25. Gould Medical Group, Inc. - Gould Medical Group, Inc. 401(k) Profit Sharing Plan and Trust 26. Garland Industries, Inc. - The Garland Industries, Inc. Employee Stock Ownership Plan & Trust 27. Tufts Medical Center Physicians Organization, Inc. - Tufts Medical Center Physicians Organization, Inc. 401(a) Retirement Plan 28. McMaster-Carr Supply Company - McMaster-Carr Supply Company Profit Sharing Trust 29. National Basketball Association - NBA-NBPA 401K Savings Plan 30. Northwest Permanente, P.C. - Northwest Permanente, P.C. Retirement Plan Money Purchase Pension Aspect --Written by Hal M. Bundrick for MainStreet

Shares Of Vringo Shoot Higher on Court Ruling

Shares of Vringo (NASDAQ: VRNG) are up roughly nine percent after a court in Virginia ruled in its favor against Google (NASDAQ: GOOG) for the period October 1st 2012 to November 20th 2012.

One of the most notable statements in the PACER doc concerns the royalty base. Vringo argued the 20.9 percent of North American revenues is fair, while Google fought for 2.8 percent.

The court document reads, "Accordingly, the Court will award supplemental damages to I/P Engine by applying a 20.9% apportionment to the revenues for the relevant time period, and then a 3.5% royalty rate," because, "the Court finds Defendants' calculation overly speculative and therefore inappropriate to rely upon."

The court also awarded Vringo prorated payments of, "$16,784,491 total, apportioned as follows: $316,408 for AOL, $137 for Gannett, $629,891 for IAC, $6,760 for Target, and $15,831,295 for Google."

Investors are still waiting for a ruling on the running rate.

Note: Luke Jacobi is long Vringo

Posted-In: News Markets Best of Benzinga

(c) 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Most Popular Solar Sector On Fire as Traders Getting More Optimistic Buffett Embarrasses Analysts Again in His Latest Big Win Oppenheimer Downgrades General Electric Benzinga's Top #PreMarket Gainers iPhone China Mobile Sales Predictions, Facebook Saves a Life & Other First Week of January Highlights Benzinga's Top #PreMarket Losers Related Articles (GOOG + VRNG) iPhone China Mobile Sales Predictions, Facebook Saves a Life & Other First Week of January Highlights Benzinga's Top Stocks Under $5 for 2014 Shares Of Vringo Shoot Higher on Court Ruling Google Clinging to Major Support Level Why Don't Android Users Buy More Stuff? Market Wrap For January 2: Markets Begin 2014 on Negative Note Around the Web, We're Loving... Lightspeed Trading Presents: Thunder and Tubleweeds: Trading Techniques for the New Market Enviroment Pope Francis Rips 'Trickle-Down' Economics Come See How the Pro's Trade in this Exclusive Webinar Wynn, MGM, Other Casino Giants Vying For U.S. Turf What Should You Know About AMZN? View the discussion thread. Partner NetworkSaturday, December 27, 2014

Ford Focus EV Under Investigation for Serious Sudden Stalling Claims

A series of consumer complaints against a popular electric vehicle has prompted an investigation by regulators.

A series of consumer complaints against a popular electric vehicle has prompted an investigation by regulators.

Documents from the National Highway Traffic Safety Administration (NHTSA) indicate that the agency is looking at about 1,000 Ford (F) Focus EVs. The investigation was sparked by a dozen reports from consumers of sudden vehicle stalling, Reuters notes.

GM Recalls Nearly 300K Chevy Cruzes for Brake Issue

Ford says that it is cooperating with the investigation, which could potentially lead to a recall.

The agency says that the complaints were made within the last five months. The stalling events were not linked to any accidents and no injuries have been reported.

Vehicles from the 2012 and 2013 model years are affected by the preliminary investigation. In about half of the reports, the vehicles stalled while traveling at speeds greater than 30 miles per hour.

In July, Ford trimmed the base price of the Focus EV by $4,000, echoing similar price cuts by other electric vehicle manufacturers.

The company has recently announced plans to install charging stations at its U.S. offices and factories to encourage electric vehicle use by its workers.

Shares of Ford rose almost 1% in Monday morning trading.

Thursday, December 25, 2014

Why I Own Rackspace

Rackspace Hosting (NYSE: RAX ) has seen share prices plummet 48% in just five months. Many investors glanced at the roller-coaster chart and decided to cash out, but Fool contributor Anders Bylund ran in the opposite direction.

In this video, Anders explains how this price drop unlocked an irresistible buying window for him, and what sets Rackspace apart from commodity rivals such as Amazon.com (NASDAQ: AMZN ) .

The amount of data we store every year is growing by a mind-boggling 60% annually! To make sense of this trend and pick out a winner, The Motley Fool has compiled a new report called "The Only Stock You Need to Profit From the NEW Technology Revolution." The report highlights a company that has gained 300% since first recommended by Fool analysts but still has plenty of room left to run. To get instant access to the name of this company transforming the IT industry, click here -- it's free.

Editor's note: The volume level in this video is variable. We apologize for the inconvenience.

Wednesday, December 24, 2014

Soybeans End Day Lower, Soybean Oil Ends Higher

March Soybean futures ended Friday's choppy trading session recovering some early losses and settled down 4¾ cents at $1038½.

March Soymeal Futures closed down 1.9 at $352. March Soybean Oil ended the session 0.08 higher at $32.16.

Front month January Soybeans ended the day at $1030½, down 4½ cents. July Soybeans closed at $1052, down 4 cents.

Posted-In: Futures Commodities Markets

© 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Related Articles Tesla Unveils Its First Battery Swap Station NY Soft Commodities End Quiet Day Of Trading Mixed Nike Analyst Roundup Following Q2 Earnings AdvisorHUB Issues Response to Reuters Article Bank Of America Weighs In On Cisco Systems, Linear Technology Orexigen Therapeutics Gains On Diet Pill Nod From European Committee Around the Web, We're Loving... World Cup Championship of Binary Options! Huanity's Last Great Hope: Venture Capitalists Don't Miss The Next Webinar to Advance your Trading Will Apple Redefine How We Shop? What Did Josh Brown Say On Our Morning Show? We're Now Hiring Journalists for our Newsdesk!Tuesday, December 23, 2014

Market Wrap-up for Dec. 22 – The Worst-Performing Dividend Stocks of 2014

While major equities indexes are almost certain to register solid gains for the year, the markets have seen plenty of turmoil as well. Here are the worst-performing dividend stocks of 2014.

The Ground RulesBefore diving into the list, let’s first establish some ground rules for our study. Here are the screening rules I used to come up with the list of laggards:

Stock must be a current dividend payer, and still trading on the NYSE/NASDAQ/AMEX Stock’s market cap must be greater than $100 million Stock must be a traditional equity (for our purposes, we’ll exclude ETFs and other funds) Stock must have lost at least 50% of its value year-to-dateNow that we have our simple rules in place, let’s see what stocks were the biggest disasters of the year so far.

The Worst of the Worst| Walter Energy | (WLT  | 1.48 | -91% |

| Cliffs Natural Resources Inc. | (CLF | 6.69 | -74% |

| Penn West Petroleum Ltd | (PWE | 2.33 | -72% |

| Mid-Con Energy Partners LP | (MCEP | 6.51 | -72% |

| Portugal Telecom S.A. | (PT | 1.26 | -71% |

| Barrett Business Services | (BBSI | 28.75 | -69% |

| Nu Skin Enterprises | (NUS | 43.55 | -68% |

| Valhi Inc. | (VHI | 5.66 | -68% |

| Companhia Sider | (SID | 2.11 | -66% |

| Carbo Ceramics | (CRR | 42.34 | -64% |

| Navios Maritime | (NM | 4.18 | -63% |

| Safe Bulkers, Inc. | (SB | 3.97 | -62% |

| Breitburn Energy Partners L.P. | (BBEP | 7.82 | -62% |

| Comstock Resources Inc | (CRK | 7.23 | -60% |

| SandRidge Mississippian Trust | (SDT | 3.66 | -60% |

| Linn Energy LLC. | (LINE | 12.24 | -60% |

| Investors Bancorp, Inc. | (ISBC | 11.02 | -57% |

| Eagle Rock Energy Partners L.P. | (EROC | 2.58 | -57% |

| Arch Coal | (ACI | 1.93 | -57% |

| Arcos Dorados Holdings | (ARCO | 5.27 | -57% |

| Peabody Energy | (BTU | 8.55 | -56% |

| LRR Energy L.P. | (LRE | 7.49 | -56% |

| TransGlobe Energy Corporation | (TGA | 3.7 | -56% |

| Enduro Royalty Trust | (NDRO | 5.38 | -56% |

| Gerdau S.A. | (GGB | 3.58 | -54% |

| Pacific Coast Oil Trust | (ROYT | 5.8 | -54% |

| Baytex Energy Corp | (BTE | 17.96 | -54% |

| SM Energy Co. | (SM | 38.76 | -53% |

| Legacy Reserves L.P. | (LGCY | 13.28 | -53% |

| Yamana Gold | (AUY | 4.1 | -52% |

| Sturm, Ruger & Co., Inc. | (RGR | 34.85 | -52% |

| W&T Offshore Inc. | (WTI | 7.63 | -52% |

| Whiting USA Trust II | (WHZ | 6.49 | -51% |

| Chicago Bridge & Iron | (CBI | 41.3 | -50% |

| National Resource Partners L.P. | (NRP | 10.04 | -50% |

| SandRidge Mississippian Trust II | (SDR | 4.5 | -50% |

Unsurprisingly, the vast majority of the stocks in this dubious list are energy-related. U.S. coal producers in particular have had a horrendous year, with many of them seemingly facing bankruptcy. You’ll also notice many MLPs in the list, which have been hammered amid the recent oil price plunge.

A couple of foreign stocks also stand out, namely Portugal Telecom (which can’t catch a break even though it’s on the verge of being acquired), and Arcos Dorados (which has been plagued by weak performance in its McDonald’s franchises, as well as negative effects from the stronger U.S. dollar).

Dishonorable mentions include SeaDrill (SDRL![]()

![]() ) and Herbalife (HLF

) and Herbalife (HLF![]() ), both of which suspended their payouts earlier this year.

), both of which suspended their payouts earlier this year.

Speaking of dividend suspensions, some of the stocks above are facing the possibility of eliminating their dividend programs in 2015. I wouldn’t be at all surprised to see stocks like WLT, CLF, ACI, and AUY suspend their dividends next year.